Commercial Property Owner Search Instantly Identify the Owner of Over 709,000 Commercial Properties

Institutional investors have long understood that the UK commercial property market is opaque. But until now, the degree of that opacity — and the startling concentration hiding within it — has been largely invisible — because the tools available for a basic commercial property owner search have been fundamentally inadequate.

Retail Store Analytics: Top 5 Insights from the UK’s Commercial Property Landscape

The UK retail property market is a vast and dynamic ecosystem. With over 788,000 shop-related commercial properties recorded across England and Wales, understanding the patterns of rental values, property sizes, occupancy, and geographic distribution is essential for investors, retailers, and policymakers.

The Missing Commercial Owner Occupier Signal in Commercial Property Underwriting

Every commercial insurer knows that the risk profile of a property is not determined by its bricks and mortar alone. The occupant — their legal status, financial resilience, operational behaviour, and tenure — is frequently the dominant variable in claims frequency, business interruption severity, and liability exposure.

Beyond the Asking Price: How Commercial Real Estate Valuation Data Unlocks the True Worth of Commercial Property

At Doorda, our Commercial Real Estate dataset doesn’t just tell you what a property is — it gives you the financial and valuation infrastructure to understand what an asset is worth, how it performs, and where the opportunity really lies.

The Hidden Goldmine: Why Commercial Occupant Intelligence is Redefining Property Analysis

When you think about commercial property data, what comes to mind? Square footage, rental values, location coordinates, and rateable values probably top the list. And for good reason — these physical and financial attributes form the bedrock of property analysis.

Commercial Property Data UK

Doorda’s Commercial Property Data UK product provides comprehensive, granular insights into over 2.5 million commercial properties across the United Kingdom.

Commercial Rental Values Repriced: What the 2026 Update Reveals for the UK Property Market

The release of the 2026 rating list from the Valuation Office Agency offers more than a routine update to business rates. It provides one of the clearest, most comprehensive snapshots of commercial rental values in England and Wales.

A Tax System Rewired — What the 2026 Business Rates Revaluation Signals for the UK Economy

The 2026 business rates revaluation has been framed as a routine update to the UK’s commercial property tax system. In reality, it represents something more consequential: a recalibration of how the state measures—and taxes—economic activity in a post-pandemic economy.

Business Rate Changes 2026: Top 10 Facts Every Commercial Property Professional Should Know

The business rate changes 2026 mark a major reset for the UK commercial property market. With the latest dataset from the Valuation Office Agency (VOA) now integrated into Doorda, users can access a fully updated view of rateable values across England and Wales.

Commercial Property Valuation in 2026: Why Data Accuracy Is the New Competitive Edge

Ask any surveyor, lender, or institutional investor about the state of Commercial Property Valuation in 2026, and you’ll hear the same refrain: accuracy has never been more critical — or harder to achieve.

Top 10 Areas hardest hit by cost of living crisis in England revealed

The areas hardest hit by cost of living crisis in England are concentrated in both inner London and post-industrial towns in the North, according to new analysis of the English Indices of Deprivation.

Top 10 Areas hardest hit by cost of living crisis in Wales revealed

Using the latest Welsh Index of Multiple Deprivation, the findings highlight neighbourhoods where households are already under significant financial strain—whilst energy tariffs are falling in April they are expected to increase in July 2026.

Who Is Barbara Kahan? What Company Director Risk Data Reveals About One of the UK’s Most Prolific Directors

With more than 45,000 directorships, she is often cited as one of the most prolific directors in UK corporate records. But who is she—and what does her presence reveal about how companies are formed and structured in the UK?

The Hidden Network Behind UK Business: What Company Director Data Reveals

Did you know that one individual holds 45,031 directorships? Or that a single organisation connects to nearly 7,000 directors? This is the reality uncovered through Doorda’s unique company director dataset (DirectorX).

Why High-Quality Corporate Intelligence Data Is Essential for Enterprise AI

For organisations exploring AI applications in corporate data, access to well-structured director data and corporate relationship datasets can significantly accelerate development while improving model reliability.

AI Evaluation Framework for Corporate Data

AI evaluation has become a critical discipline for enterprises deploying machine learning models on corporate intelligence datasets. Without structured model validation and rigorous AI quality assurance, AI systems can produce misleading insights.

Top 20 Private Landlords: Who Owns UK Housing and Why It Matters

Large private landlords in the UK are typically profit-driven companies that appear frequently as registered property owners in title data.

Top 20 Pub Operators by Pub Business Rates Bill: Who Pays the Most?

Pub business rates remain one of the largest fixed costs facing the UK pub sector. With pub business rates due to rise again from April, and only partial relief available under the government’s latest concessions, operators are bracing for yet another squeeze on margins from rising pub business rates bills.

Unlocking Strategic Insights from CMA Regulatory Oversight Data

In today’s complex and rapidly shifting business environment, companies face mounting pressure to remain compliant while navigating increasingly competitive markets.

Using Court Judgement Intelligence to Transform Compliance Monitoring

In today’s regulatory environment, compliance monitoring has become far more than a box-ticking exercise.

50 Largest Warehouses in the UK: Inside the Country’s Biggest Distribution Centres

Using commercial property and business rates data, we’ve analysed some of the largest distribution centres and logistics hubs in the country, highlighting where they are, who operates them, and why they matter to the UK economy.

New AML Compliance Dataset Contains 2,208 penalties

As regulatory expectations continue to rise, organisations need more than policy documents and best-practice checklists to stay compliant — they need real-world intelligence.

The Hidden Risk in Your Supply Chain: Why Every Business Needs Tax Avoidance Intelligence

In today’s regulatory landscape, partnering with the wrong company can cost your business far more than a failed deal—it can damage your reputation, trigger regulatory scrutiny, and expose you to significant compliance risks.

Doorda Secures US Patent, for Breakthrough Address-Matching Technology

A major milestone highlights how Doorda is redefining global standards in address accuracy, speed, and reliability.

The £2 Million Property Tax: Where the Shockwaves Will Hit First

The £2 million property tax will undoubtedly reshape parts of London. But its ripples will extend far beyond the capital, affecting affluent commuter towns, regional cities.

Company Compliance Intelligence for Business Lenders and Insurance Underwriters

Companies with patterns of environmental violations, employment tribunal losses, or health and safety breaches represent significantly elevated risks that don’t appear in financial statements alone.

New Dataset: Risk Tax Defaulter

The tax defaulter dataset is a comprehensive registry of companies that have failed to meet their tax obligations, providing critical intelligence on corporate tax compliance failures.

How to Leverage Property Data for Accurate Market Forecasting

Gain deeper insight into the UK housing market using data from 22.5M properties. Learn how property analytics improves forecasting, pricing, and investment decisions.

2M+ UK Properties with Company Registrations: Corporate Location Intelligence Property Data

For organisations consuming property data, the message is clear, property data is business data. When combined with the 100+ attributes available — from named occupants to ownership and spatial metrics — it becomes a powerful foundation for risk insight, market discovery, and strategic planning.

Britain’s Housing Giants: The Scale of the UK’s Largest Social Housing Providers

Britain’s social housing sector remains one of the most critical parts of the housing market, ensuring that millions of people have access to affordable and secure homes.

Property SDK: Build Smarter with Our Python Toolkit

Our PropertyX database provides comprehensive coverage of 34.5M commercial and residential properties. All these can now be accessed directly via our Python SDK.

Top 20 UK Planning Application Hotspots for 2025

Top 20 UK planning applications in 2025 ranked by value – Oxford, Cambridge, Birmingham, Wembley, and more shaping housing, regeneration, and development trends.

Unlocking Opportunities in the UK Construction and Planning Sector

The UK construction and planning ecosystem is more vibrant—and more competitive—than ever. Behind every major development, a complex network of companies and professionals shapes everything from city skylines to rural infrastructure.

Turning Large Planning Applications into Competitive Advantage

For insurers, developers, and market analysts, knowing where and what is being built can be the difference between getting ahead of market shifts—or missing them entirely.

Unlock the Power of Local Planning Intelligence

When it comes to property, planning, and research, smart decisions start with trusted, timely data. At Doorda, we empower professionals with the UK’s richest planning and property datasets.

5 Reasons Why Doorda AI Makes Planning Application Data Work Harder

If you’ve ever wrestled with planning applications, you’ll know the data is there — but finding the story in it is another matter.

Understanding the Limits of Flood Re’s Property Tax Band Data

In the world of insurance, access to accurate, property-level data is crucial — not just for risk assessment but increasingly for building richer, more predictive models.

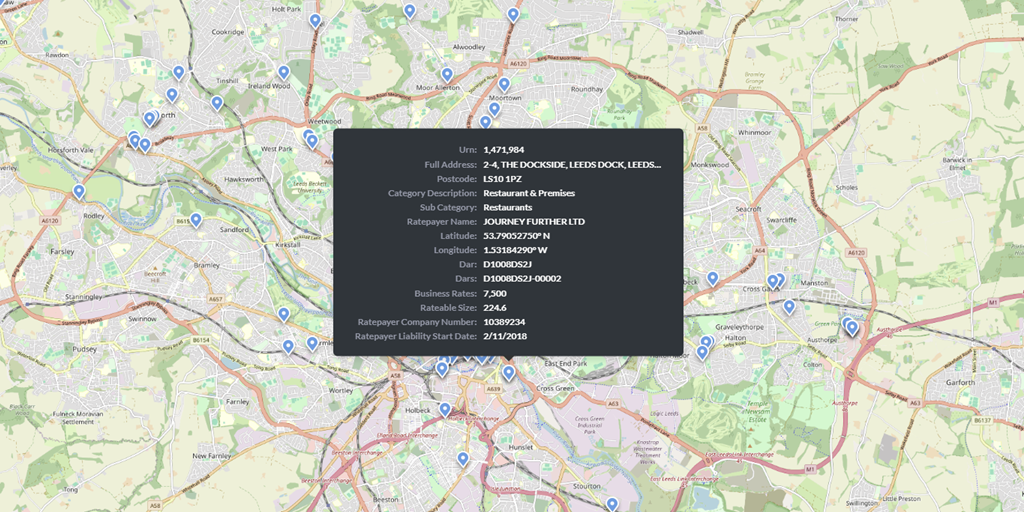

Instant Access to Smarter Commercial Property Data

Available instantly via DoordaOnline—our browser-based platform—CommercialX makes it easy to access, search, and filter data without any technical expertise.

Doorda AI for Commercial Property Insight

In today’s fast-paced world of commercial insurance and property investment, one thing is certain: traditional data sources and manual analysis no longer cut it. Risk is dynamic.

New Release: GDPR-Compliant Council Tax Band Data — Now Available

Organisations can now access a single, comprehensive dataset of UK Council Tax bands and precepts — clean, structured, and ready to use. If you’ve ever tried to gather Council Tax data across the UK, you’ll know it’s one of the most fragmented datasets in the public domain.

Non-Compliant Council Tax Band Data is a Legal Risk!

Organisations are always on the lookout for high-quality datasets to improve customer insight, build smarter models, and gain a competitive edge. But not all data that looks public is legally safe to use.

Council Tax Bands: A Hidden Asset for Business Intelligence

For many, council tax bands are just part of a household bill. But for businesses and analysts, they represent something much more valuable…

Fixing the Fragmented Landscape of UK Council Tax Band Data

In the world of open data, few public datasets expose systemic dysfunction quite like UK Council tax bands.

Hidden property data that Insurers and Marketers can’t afford to ignore

What if you could understand not just where a property is, but when it was built – and what that says about risk, opportunity, and consumer behaviour?

How Doorda’s Procurement Data Can Help Lenders, Insurers and Underwriters

In today’s volatile credit environment, invoice insurers, underwriters, and lenders need every edge to stay ahead of risk. Analyse all government, local authority and NHS procurement above £12,000.

Locking Down MoT risks: The Power of Location & Operator Data

Our new licensed MoT garages dataset isn’t just a list of garages—it’s an intelligence opportunity.

Why Government Spend Data Is a Game-Changer for Your Business Strategy

In an era where data rules decision-making, tapping into every available insight is essential. Yet one of the richest, most underexploited sources remains government spending data.

A Brief History of Government Spend Data

Since the early 2010s, the UK has led the way in using open data to hold public bodies to account with all local authorities and government bodies now required to publish invoice level data.

£1.8m in claims a day! The Role of Hard Water and Its Impact on Properties

Water escape, or “escape of water,” remains a persistent challenge in the UK, causing significant damage to properties and leading to costly claims for insurers and underwriters.

Explore all our data products via DoordaOnline

Our new user-friendly, web-based interface is designed to simplify data exploration and querying, making it much easier to access 100s of datasets efficiently and intuitively.

Weaknesses in public data threatens predicted AI gains

The rapid growth of artificial intelligence faces significant threats due to a shortage of high-quality data, a fundamental issue restricting AI’s potential across numerous sectors.

Water Damage Risk Modelling with Water Hardness Data Linked to Postcodes

Water Damage Risk Modelling can easily be enhanced with a detailed dataset linking UK water hardness levels to 1.6M postcodes providing valuable insights for insurance companies and those interested in property.

Top 20 UK Commercial Property Owners by Physical Footprint (2025)

Top 20 UK Property Owners by Floor Space 2025 | Amazon Leads

Top 20 Commercial Property Owners in the UK by Rateable Value 2025

Discover the top 20 UK commercial property occupants in 2025. Data from Doorda shows supermarkets like Tesco, Lidl & Aldi dominate by rateable value.

Unlock Deeper Insights into Commercial Locations

We are thrilled to announce the launch of CommercialX, offering comprehensive insights into over 6 million commercial properties across the UK.

National Data Library, the way forward

Supporting the UK Government’s National Data Library Initiative

Navigating the Economic Crime and Corporate Transparency Act

Upcoming Changes in the Economic Crime and Corporate Transparency Act: What Data Consumers Need to Know

Unveiling DirectorX: Precision Insights for Smarter Marketing & Compliance

In today’s business landscape, data is a powerful asset that enables better decision-making, drives strategic marketing, and supports regulatory compliance. That’s why we’re thrilled to introduce our new Director Data Product.

Guiding Companies Toward Climate Action and Compliance

The Science Based Targets initiative (SBTi) is an organization that helps companies and financial institutions set goals to reduce their greenhouse gas emissions

Grey Data isn’t Good for Business

Using scraped or grey data for building data models can present several risks and ethical concerns, which is why it’s generally advised to avoid relying on such data.

Address Insights Reimagined

In today’s dynamic business environment, particularly within the retail, real estate, and service sectors, leveraging precise location data has become indispensable.

Point Sigma Improve AI-driven Analytics

Identifying and swiftly responding to data-driven insights across a range of needs from marketing and credit risk through to customer service and collections is now a common, business critical requirement.

Stop Scraping Open Data!

Looking back into the deep dark days of the early web Before the advent of open Apis Schema.org and RDF, and definitely, well before Artificial intelligence, visual web scraping was one of the very few ways to get structured data out of the web.

Why Data Management is far from ‘NIRVANA’.

Using external data, in particular, to enrich context, improve accuracy or broaden scope matters significantly if data practitioners are to deepen insights, improve predictions, or personalise offerings.

What does chronological age mean?

Chronological age is a concept that measures the number of years a person has been alive since birth, chronological age forms the basis of our understanding of time and aging.

Comparable Areas, OA or LSOA?

Lower Super Output Areas (LSOA) fit within Local Authority boundaries and Output Areas (OA) fit within an LSOA. These were originally developed as part of the census to allow for comparison across different parts of the country.

Experienced data buyers discover Doorda via Nomad Data

Doorda, a UK data provider specializing in property, business, and geo-demographic data, has partnered with Nomad Data to discover sophisticated data buyers

Insuretechs look to Doorda to construct better client and risk profiles

Doorda provides the insurance sector, from brokers and underwriting platforms to established tier-one insurers, with reliable UK data to improve assessments and recommendations.

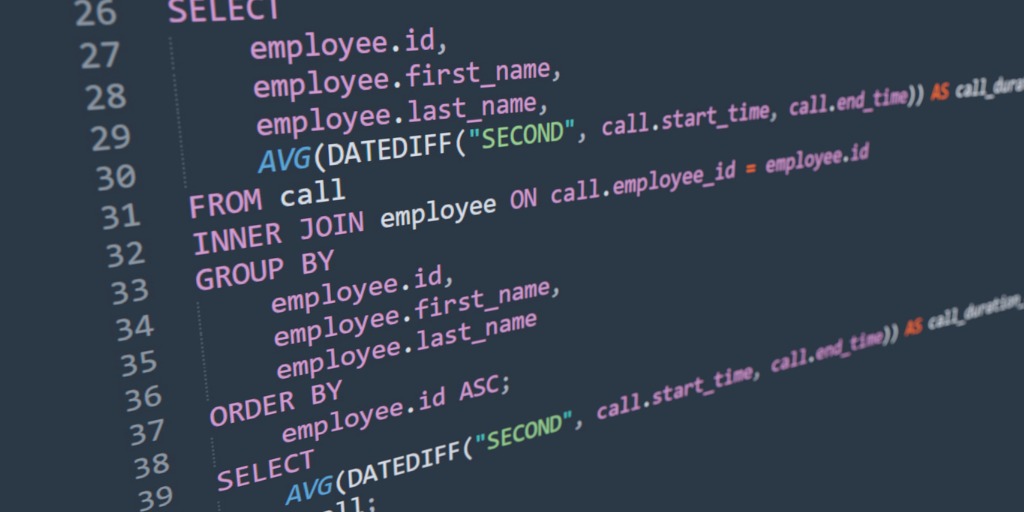

Using INNER JOIN versus CROSS JOIN in SQL

Using the right JOIN statement in your SQL code is critical for accurate results. While it might be easy to identify a bad data set when only a few results are returned, it’s not so easy when you have thousands of results.

Should You Use NULL values in Your SQL Database?

If you search for NULL standards in Google, the first page shows you answers from both sides of the debate. Using NULL values in your database is a permanent choice. Once you choose to allow them, you need to allow NULLs in all SQL database tables.

Government and Open Data for AI Start Ups

AI and machine learning start-ups are some of the most exciting and interesting businesses out there today. They are curing diseases, trading trillions of pounds of stock, and making sure your home assistant can understand what you want when you say “OK Google”.

4 Useful Tips for Working with R and RStudio

Working with R and RStudio can be very rewarding as R is one of the most powerful data processing and data visualization programming languages available.

Smoking rates across the UK

Whilst smoking rates are trending downwards nationally there are still pockets where smoking greatly exceeds expected averages. In 2018, 14.7% of people aged 18 years and above smoked cigarettes.

Your biological age can go into reverse

Biological age refers to how old your body seems, based on various physical and functional markers, rather than just counting the years you’ve been alive.

Life expectancy, who wants to live forever?

Life expectancy is a statistical measure that estimates the average number of years a person is expected to live based on various factors such as their birth year, gender, and the overall health and living conditions of a population.

Identify the best locations for new stores using data

Data is a cornerstone of effective location analysis, providing critical insights for businesses aiming to make informed decisions about where to establish their presence.

4 easy ways to Optimize SQL Queries and Enhance Security

The fastest way of improving response times is to Optimize your SQL Queries. Your backend SQL server be it MYSQL or Microsoft is the powerhouse of application performance.

What Our Customers are Saying

“Doorda was differentiated given their unique proposition”

Nigel Wilson

Partner, Deals Insight & Analytics, PWC

“We had to acquire masses of data about the local population as soon as we could”

Vivienne Parsons

Specialist Business Analyst, South Central Ambulance Service

“The new partnership gives our clients more available depth within our existing data products”

Kelly Preston

Managing Director of 118/Market Location

“Doorda has become a trusted data partner and we think there’s a lot more we can do together”

Scott Logie

Customer Engagement Director, Sagacity

“Doorda brought us data we hadn’t seen before”

Mao Ruijia

Lead Growth Analyst, Capital on Tap

“The acceleration in time to value for CARTO customers is a clear win-win.”

Luis Sanz

CEO, CARTO

“Doorda excels in providing the detailed, raw data that is so key”